NOTE: Thank you for supporting this sponsored interview, which helps keep this broadcast running to bring you uncensored news.

Back in the late 1990s, Americans were told the internet was the future, and they were right.

The internet really did change the world forever.

But Wall Street took a legitimate technological revolution and turned it into one of the greatest speculative bubbles in financial history. Companies with no profits, no viable business model, and sometimes barely any revenue were suddenly worth billions. Pets.com became famous for losing money selling dog food online. Webvan burned through more than $1 billion trying to revolutionize grocery delivery before collapsing. eToys skyrocketed despite never building a sustainable business.

None of it mattered because investors were told one thing over and over again: Get in now or be left behind forever.

The NASDAQ surged nearly 400%+ between 1995 and March 2000 as Americans poured retirement savings into tech stocks they barely understood. Analysts insisted the old rules no longer applied because the internet was “changing everything.”

And again, they weren’t entirely wrong. The internet did change everything.

But the profits investors were pricing into those companies were built almost entirely on speculation rather than sustainable business models.

Then reality hit. After peaking at roughly 5,048 in March 2000, the Nasdaq collapsed to around 1,140 by October 2002, wiping out almost 80% of its value and trillions in wealth.

Retirement accounts were crushed. Many of the hottest companies of the era disappeared completely.

And now, it feels like history is repeating itself all over again, only this time with artificial intelligence.

AI has become the new gold rush on Wall Street. A tiny cluster of AI-driven tech companies now accounts for a massive share of the gains powering the entire stock market. In fact, AI-related enthusiasm has driven a huge portion of the S&P 500’s gains over the past two years, largely concentrated in a handful of mega-cap tech firms.

Billions upon billions are now being poured into AI infrastructure, chips, data centers, and speculative valuations based largely on future promises rather than proven profitability. And when you look under the hood, the numbers don’t match the hype.

OpenAI (the face of the AI boom) generated around $3.7 billion in revenue in 2024, scaling up to $20 billion in 2025.

But despite that explosive growth, the company is still spending so much on computing power, chips, servers, and data centers that it won’t be anywhere near profitable anytime soon.

Sam Altman himself referenced commitments of about $1.4 trillion in data center and compute infrastructure spending over the coming years (primarily 2025–2033).

A $20 billion annualized revenue run rate sounds impressive on the surface. But when your spending commitments are in the trillions, many analysts question whether this is a sustainable business model.

At the same time, businesses everywhere are racing to integrate AI into daily operations, yet a National Bureau of Economic Research study shows that roughly 90% of executives report little to no measurable impact on productivity or employment over the past three years.

That doesn’t mean AI is fake. Just like the internet, AI will likely transform society in very real ways. But transforming society and justifying trillion-dollar speculative valuations are two completely different things.

Because right now, enormous amounts of wealth are being priced on assumptions about what AI might become someday. And if history has taught us anything, it’s that you do not bet the farm on speculation.

Especially when the entire financial system is already drowning in debt.

So what happens next when the most overhyped sector in the market finally bursts while the broader financial system is already hanging on by a thread?

And what happens when the same institutions driving the AI boom also push society deeper into digital IDs and centralized bank digital currencies (CBDCs), where access to your money can increasingly be monitored or controlled?

Because if the old financial system breaks under the weight of speculation and debt, many fear the solution waiting on the other side won’t be less centralized control. It will be more.

Bill Armour from Genesis Gold Group joins us to discuss.

The heart of the fear surrounding AI is not really about robots or futuristic technology. It is about what happens when enormous amounts of money, power, and decision-making become concentrated into fewer and fewer hands while millions of ordinary people become economically disposable.

Bill Armour argued that Wall Street is treating AI the same way it treated the dot-com boom, except this time the scale may be even larger. Investors are flooding into anything connected to AI because the market believes it represents the next great technological revolution. In many ways, it probably does.

The problem is that speculation moves faster than reality.

Armour pointed out that many companies are already slashing jobs and restructuring entire departments around AI despite little evidence that the productivity gains actually justify the hype yet. A National Bureau of Economic Research study found that roughly 90% of executives reported little or no measurable impact from AI over the past three years, yet companies are still racing to replace workers preemptively.

That is where the issue becomes deeply personal for ordinary people.

Modern economies rely on millions of middle-class consumers continuously working, borrowing, spending money, paying taxes, and servicing debt. When large portions of those jobs disappear all at once, the entire system starts destabilizing from the bottom up.

Armour warned that people are underestimating how quickly this could happen because AI grows exponentially, not linearly.

“If AI disrupts labor faster than society can adapt, the debt math breaks,” he explained.

The danger is not simply unemployment. It is what unemployment does to a heavily indebted financial system already stretched to the breaking point.

People default on loans. Banks absorb losses. Companies lose customers because consumers cannot afford products anymore. Smaller firms collapse and get absorbed by larger corporations, further consolidating economic power.

The result starts looking less like free market capitalism and more like a system where survival increasingly depends on access controlled by a small group of institutions and mega corporations.

Armour described it bluntly:

“We really do enter into the kinds of systems we’ve talked about on the show many times, which is you’ll own nothing and be happy because again, you don’t have access to income and any job or work that you can do, the jobs are so limited that the power then shifts dramatically to this elite class.”

What unsettles many people is how familiar some of these patterns already feel. Entire industries are consolidating. White-collar workers increasingly fear automation. Younger generations are openly hostile toward parts of the AI rollout because they see their future becoming more uncertain, not less.

And unlike past technological shifts, many fear this transition may happen too quickly for society to adjust before the damage is already done.

While the public is being encouraged to pour money into AI-driven markets, major financial institutions appear to be preparing for something very different behind the scenes.

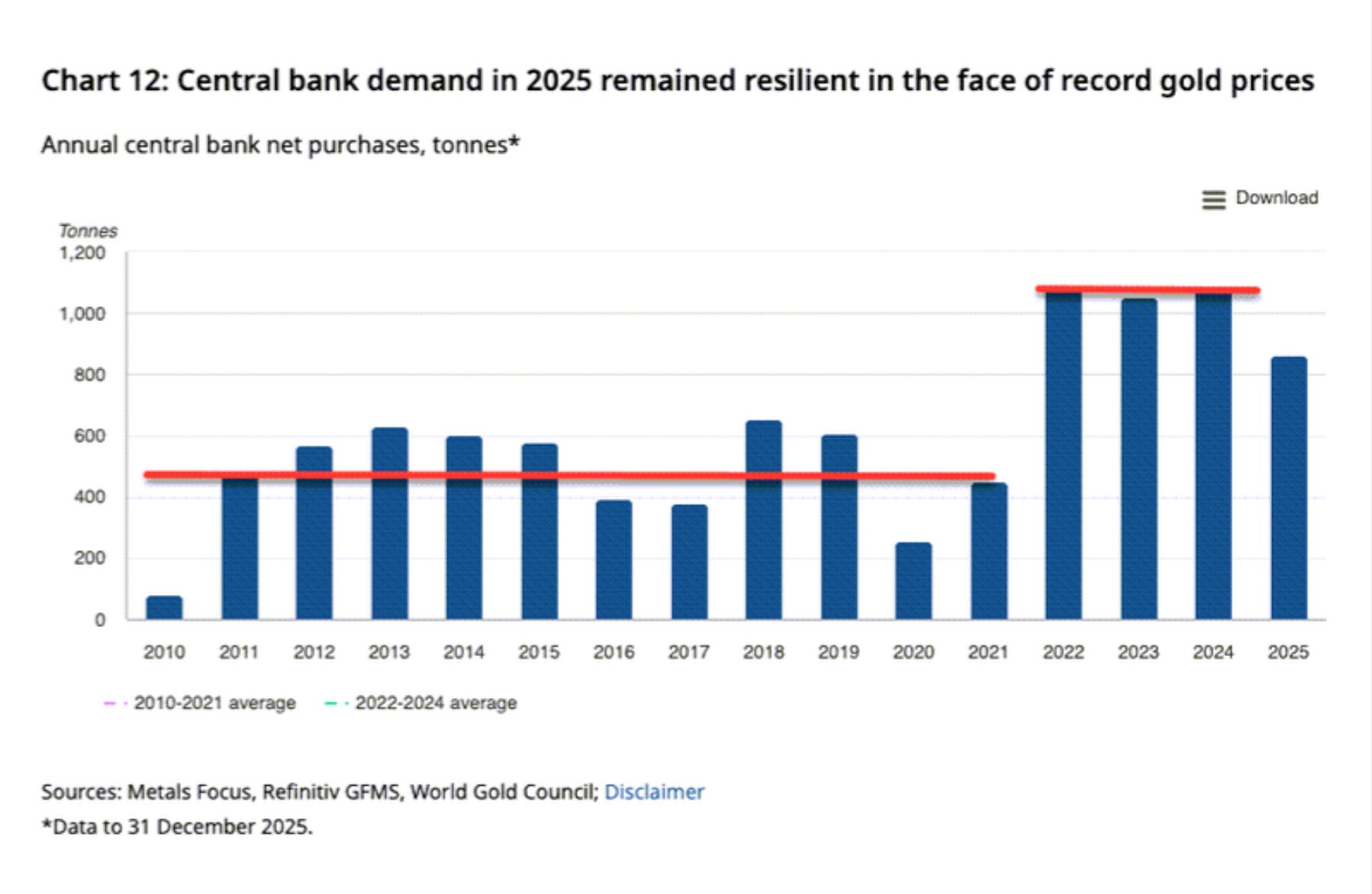

Maria Zeee pointed to central banks and major institutions rapidly accumulating physical gold while simultaneously promoting speculative paper markets to ordinary investors.

JP Morgan and HSBC have both moved massive quantities of gold into vaults as confidence in the long-term stability of the financial system continues eroding globally.

Armour argued that people should pay less attention to what powerful institutions say and more attention to what they are actually doing.

“Don’t buy what the banks are selling. Buy what the banks are buying.”

Both Maria and Armour pointed toward the growing infrastructure surrounding digital identity systems, centralized digital currencies, and AI-powered surveillance technologies. In their view, a large enough economic crisis could create the perfect environment for governments and institutions to roll out systems that would have previously faced massive public resistance.

Armour referenced companies like Palantir and warned that AI now makes forms of mass surveillance possible at a scale that would have sounded unrealistic just years ago.

“I mean, literally every single person in the country [could be monitored] at the exact same time.”

Maria connected those fears directly to real-world examples people have already witnessed, particularly the freezing of bank accounts during Canada’s Freedom Convoy protests.

The technology for a compliance-driven financial system already exists. And if a major financial collapse creates enough panic, it’s not hard to imagine the public accepting systems they otherwise would have strongly resisted.

Just look at the Patriot Act. It was introduced as a temporary response to a national emergency, yet decades later much of it still remains. The same thing could happen with a new digitized financial system that normalizes surveillance and control that people would never have accepted under ordinary circumstances.

Now imagine living under a system where your money is tracked, traced, and tied to compliance, then compare that to gold and silver.

Gold and silver have outlasted every paper currency experiment in human history.

Empires collapse.

Debt bubbles burst.

Governments print money.

And somehow, through every financial crisis, gold and silver continue holding value generation after generation.

Why?

Because gold is not built on trust. Paper currencies are.

And once trust in the financial system starts breaking down, everything built on that trust suddenly becomes a lot more fragile.

That’s why central banks around the world are buying physical gold at record levels…

Ask yourself honestly: Does it really feel like faith in the dollar, the banking system, or the long-term stability of the economy is increasing right now?

Or does it feel like ordinary people are working harder every year just to keep up while inflation, debt, housing costs, and financial anxiety continue spiraling higher?

That’s exactly why more Americans are turning to Genesis Gold Group to move part of their retirement savings into physical gold and silver, tangible hard assets they can actually own and control outside increasingly fragile paper markets.

Because when the financial system starts cracking, what would you rather hold: tangible gold and silver or numbers on a screen?

The rising price of gold over the last few years tells you how more and more people are answering that question.

To learn how Genesis Gold Group can help you move part of your savings into tangible assets you can actually own and control, assets that have preserved wealth for generations, visit DailyPulseGold.com now.

What happens to a person psychologically when access to their money or banking can disappear overnight?

Maria described her own experience of being ‘debanked’ simply for expressing controversial views online. No crime. No violence. No threats. Just speech.

What stayed with her most was how fast everything changed.

“You know, I’ve seen how quickly your whole life can be turned upside down by getting an email.”

That experience fundamentally changed the way she views proposals like programmable digital currencies or centralized financial systems tied to digital identity infrastructure.

Her concern was simple: if institutions already have the power to freeze or restrict access to financial services today, what happens once money itself becomes fully programmable and centrally controlled?

Armour agreed that many people are still underestimating how fast these systems could emerge during a crisis.

“When we reach that point, it’s something that looking back and in hindsight we might say, man, I saw this coming a mile away. And yet it will feel like it got here faster than you ever imagined.”

For viewers worried about becoming trapped inside systems they no longer control, Armour repeatedly emphasized reducing dependence on fully digital financial structures wherever possible.

His proposed solution centered around physical assets like gold and silver, particularly through Gold IRAs and retirement diversification strategies outside traditional paper markets.

The broader message underneath the financial advice was really about preserving flexibility and independence before panic sets in.

Because once people feel trapped financially, their ability to resist pressure, make independent choices, or challenge authority becomes dramatically weaker.

That fear goes far beyond politics or finance. It’s the fear of losing control over your everyday life.

People can barely describe it, but many feel something unsettling unfolding around them: the sense that the systems they depend on are becoming more fragile, more centralized, and harder to trust.

Part of that anxiety comes from speed.

Technology is evolving faster than social systems, governments, businesses, and ordinary workers can realistically adapt to. Entire industries are restructuring around AI before most people even fully understand how the technology will affect their own lives.

Meanwhile, national debt has exploded past $39 trillion, trust in institutions continues eroding, and financial markets increasingly feel disconnected from the reality most people live every day.

That combination creates an environment where fear spreads easily because people sense instability even if they cannot fully articulate it.

Maria repeatedly returned to the importance of preparation rather than panic. She argued that people feel less fearful once they begin taking practical steps to become more self-reliant, whether financially, technologically, or even physically through things like growing their own food.

“The more prepared I personally am, the less fearful I am.”

That may explain why so many people are becoming emotionally invested in issues surrounding AI, surveillance, digital identity systems, and financial control. For many, these topics no longer feel abstract or futuristic. They feel connected to basic questions about independence, stability, privacy, and whether ordinary people will still have meaningful control over their own lives as technology reshapes society around them.

Collapse is not guaranteed, and not every fear surrounding AI will become reality.

But major structural changes are already unfolding in real time, and by the time most people fully realize what’s happening, opting out of a future they never signed up for becomes much harder.

We encourage viewers to become ungovernable: build local connections, stay engaged with what’s happening, and take steps to preserve your financial independence before the system demands compliance.

Because the people who prepare early usually have the most options left, and therefore the most freedom.

The biggest risk in a speculative bubble is not just losing money. It’s what happens to ordinary people after the bubble bursts.

Because when financial systems start breaking down, governments and institutions rarely respond by giving people more freedom or more control.

Usually, it’s the opposite.

Right now, Wall Street is pouring staggering amounts of money into a tiny handful of AI companies while the broader financial system sits on top of historic levels of debt and instability. And if that bubble bursts the way previous speculative bubbles did, millions of people could suddenly find themselves trapped inside another financial crisis they didn’t create.

But this time, the system waiting on the other side may look very different.

We already got a preview during Canada’s Freedom Convoy.

People who supported the wrong political movement suddenly lost access to their own bank accounts. Their money became conditional on compliance.

That moment showed millions of people something they had never fully considered before:

If governments and centralized financial institutions can freeze access to money once, they can do it again.

And as digital IDs, CBDCs, AI surveillance systems, and programmable finance continue advancing around the world, more people are realizing the same thing Bill Armour warned about during this episode:

The real issue is no longer just inflation or market volatility. It’s control.

That’s where Genesis Gold Group comes in. Their team has spent decades helping families move part of their retirement savings and long-term wealth into physical gold and silver, tangible hard assets people can actually own and control outside increasingly fragile paper systems.

Unlike speculative digital assets or numbers sitting inside centralized financial networks, physical gold and silver cannot simply be printed away, digitally restricted, or frozen because of politics or compliance.

That’s one reason central banks around the world continue aggressively accumulating gold: because the more of it they control, the less ordinary people do.

As Bill Armour explained: “Don’t buy what the banks are selling. Buy what the banks are buying.”

If that logic makes sense to you, Bill and the team at Genesis Gold Group are here to help.

They’ve helped thousands of people roll over hundreds of millions of dollars into Gold IRAs and physical precious metals while guiding them step-by-step through the process with the kind of personal attention and trust that has earned Genesis an incredibly loyal customer base.

As the Freedom Convoy showed us, access to your own money can quickly become dependent on compliance. And keeping 100% of your assets inside the system makes you far easier to control.

To learn how you can move part of your savings into tangible assets you can actually own and control, visit DailyPulseGold.com today.

We want to thank Bill Armour for joining us today—and more importantly, we want to thank you for watching and doing your duty to be informed when so many others choose not to.

Follow us (@ZeeeMedia and @VigilantFox) for stories that matter—stories the media doesn’t want you to see. We’ll be back with another show tomorrow. See you then.