NOTE: Thank you for supporting this sponsored interview, which keeps this website running to bring you uncensored news.

Last week, the market did something it hasn’t done in a long time. It blinked.

The Nasdaq dropped more than 2% in a single session — its second straight day of losses.

Micron, one of the hottest chip stocks on the planet, cratered 13% in a day.

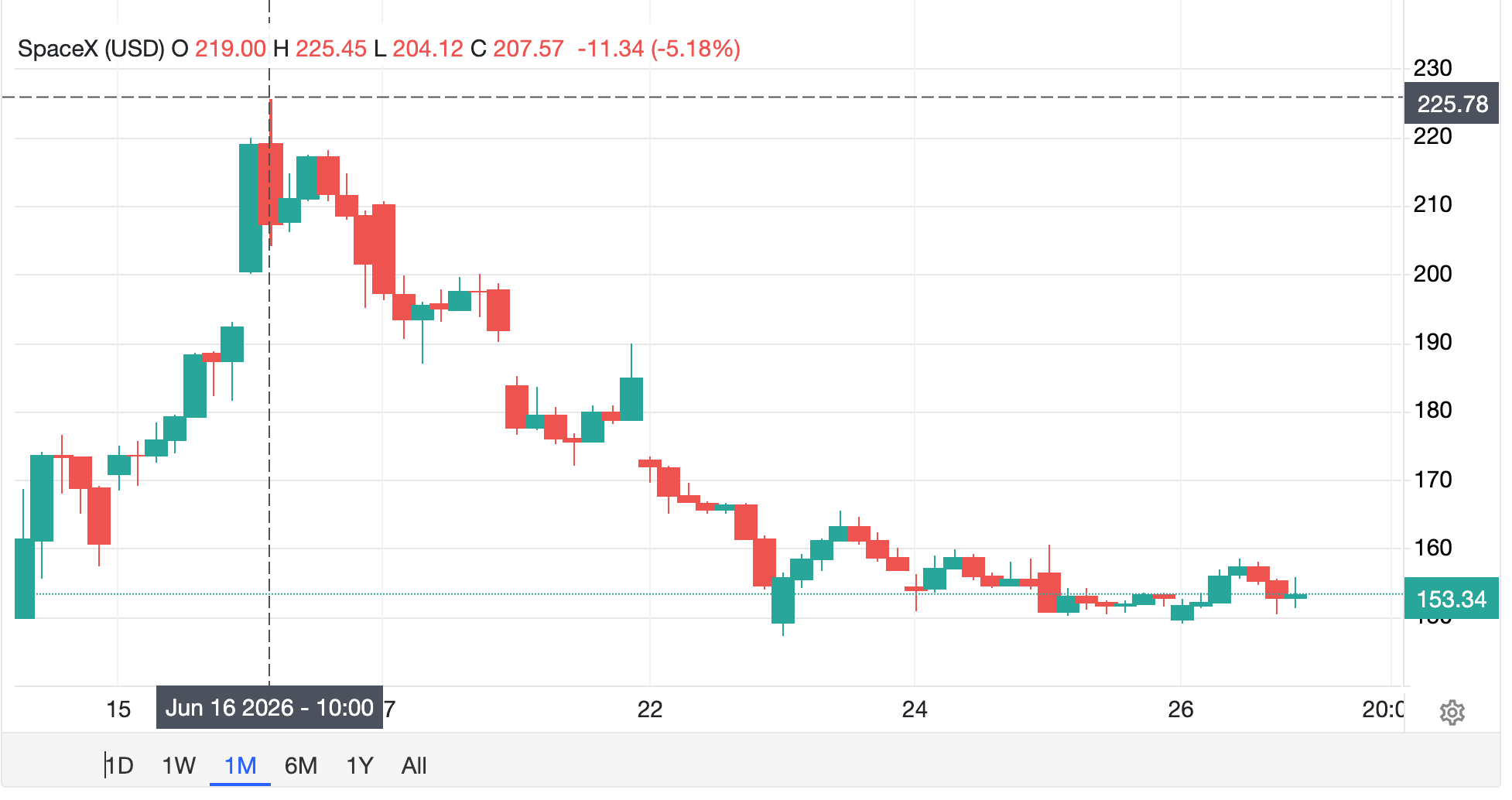

SpaceX’s total valuation shed nearly a trillion dollars from its peak. We hope you didn’t chase that one at the top.

While this is all happening, the story they’re selling you is “volatility.” A short roadblock. “Buy the dip.”

But deeper down, there is something the Jim Cramers of the world are not saying out loud.

Two of China’s biggest hedge funds just called the AI boom a giant bubble. Even Mainstream outlets are echoing those concerns.

OpenAI is burning cash faster than they can raise it. It just signaled it may delay going public until 2027 because it’s not sure regular investors will even show up.

So if the smart money’s nervous… and the companies are bleeding… where’s the money supposed to come from to keep this whole thing standing?

One man already answered that question. And you need to hear exactly what he said.

His name is Larry Fink. He runs BlackRock, the largest money manager on the face of the Earth. When BlackRock talks about where money is going to come from, they’re not guessing. They’re describing the plan.

Fink said building out America’s AI infrastructure will take $10,000,000,000,000.00 over the next decade. Ten trillion.

Where will it all come from? These are his words, not mine: “savings accounts… pension accounts… insurance companies… on and on and on.”

“Savings accounts.” “Pension accounts.” That’s not Wall Street’s money he’s talking about. That’s yours. Your retirement. Your 401(k). The pension you spent thirty years earning.

The trillions to prop up this AI bet are going to come out of your nest egg. And nobody slid a contract across the table. Nobody asked your permission.

In Australia, they’re already further down this road than we are. If you’re investing in the stock market, you’re investing in tech stocks. There’s just not a lot of choice around that.

Whether this all works or not, giant investment firms like BlackRock still collect their fees.

And if this all crumbles, it’s not their money that vanishes. It’s yours.

To break all of this down, we’re joined now by Bill Armour of Genesis Gold Group.

The head of BlackRock just told you where the money for AI is coming from: your retirement.

That’s what makes Larry Fink’s comment so dangerous. He didn’t talk in riddles — he named it out loud: savings accounts, pension accounts, insurance. Bill’s read: every so often the people running the system “almost take the mask off,” and “that’s what happened here.” Maria said what you’re already thinking: “wait a minute… you mean my money?”

Yes. Your money. And here’s the part nobody tells you: you’re already in the AI bet. You never bought Nvidia. You never touched Micron. You never placed a single trade. The person managing your 401(k) did it for you.

Here’s how. The rules were quietly loosened right before all this, opening the door for your retirement to pour into companies that lose money by the billions. OpenAI and Anthropic run at a loss on borrowed cash; as Maria put it, “the whole industry is built on debt.” Your nest egg is the fuel.

Think you’re clear because you don’t own tech stocks? In Bill’s words, “you may not have chosen this AI trade directly, but your retirement account manager, etc., probably has.” That “safe” index fund, the target-date fund you never open — they’re stuffed with the same five giants: Microsoft, Nvidia, Alphabet, Amazon, Meta. When the label says “diversified,” Bill’s question is the one that matters: “diversified into what?” Ten holdings that rise and crash together aren’t ten bets. They’re one bet, ten times over.

Pensions are worse, because people assume they can’t be touched. They can. They chase the same returns, which is how the risk gets “quietly embedded… in the things that every, every consumer purchases.”

Citing Ed Dowd, Maria noted that “45% of the S&P 500 is AI or AI adjacent” — nearly half the index you think of as safe. And when it turns, Bill warns, “regular people become the exit liquidity for the biggest speculative bet in history.” You’re who’s left holding it when the smart money runs.

So what actually happens to your account when this pops?

#ad: Unless you have explicitly told your financial advisor to pull your money out of tech, you are fully invested in the AI bubble right now.

Nobody asked for your permission. Nobody had to.

Your 401(k) is on autopilot, and autopilot means the biggest names on Wall Street get to use your retirement to fund their AI bets. Larry Fink’s BlackRock alone manages $12 trillion of money just like yours.

If it pays off, they take the fees. If it pops, you hold the bag.

But there’s a way to opt out of the AI bubble, and Genesis Gold shows you how.

They put together a free guide with the whole picture. How exposed your retirement really is. What happens after the crash. And how to get your hard-earned money out before the bomb goes off.

Get it now at DailyPulseGold.com. That’s DailyPulseGold.com.

DISCLOSURE: This ad was paid for by Genesis Gold Group. We may earn a small commission when you shop through our sponsors. Thank you for your support.

Strip AI out of the economy and the recession is already here.

Bill’s math: “97 or so percent of all GDP growth in this country is from AI capital expenditures” — companies shoveling cash into their own AI divisions. Take that away and growth flatlines. His bottom line: “We would be in a full-blown recession right now if not for the AI sort of spending.”

So the whole economy rides on one assumption: that the spending turns into profit. If it doesn’t, companies stop spending, GDP stalls, and share prices “drop precipitously.” The recession just shows up late.

Here’s who eats it — and it’s not the people who built this. In 2008, Wall Street protected itself and Washington made sure “they get their golden parachutes.” The bill rolled downhill. Same script now: “the average everyday American is the one that’s going to take the hit,” gutted in the accounts he was quietly signed up for as the hedge funds cash out and move on.

Then the second punch. The Fed steps in to stop the bleeding — printing money, the 2008 playbook — and the dollars in your wallet buy less. Your account shrinks and your paycheck weakens at the same time. Bill calls it what it is: “a two-pronged approach to attacking your savings.”

Anyone shrugging this off, he says, is “being naive, if not something beyond that.”

But a crisis this convenient never arrives without the fix already prepared.

When it crashes, Bill argues, the “solution” is already written — and it costs you control of your own money.

First, the bailout. He calls a government rescue of the AI giants “a foregone conclusion” — the 2008 bank rescue run back for companies now branded national security. Can’t let China win, so we can’t let them fail. And these are the same firms, he notes, bankrolling “just about every major politician’s run.” Who covers it? You do. Washington papers over the losses by printing new money — and Bill puts it flatly: “all they’re doing effectively is stealing from the American public.”

Then, the pitch. A wiped-out public, he warns, is an easy sell for a system offering “a little more control.” The pattern he traces: “an event, in this case a crash, creates fear, fear creates dependence, and then dependence creates acceptance.” The product on offer is a central bank digital currency, rolled out “under the guise of safety or efficiency.” He points straight at the COVID playbook: “don’t do any research, just trust us.”

Maria says the wiring is already going in. She counted “80 bills right now across all of the states that are all digital ID related,” plus age-verification laws she reads as the on-ramp. What makes it work, Bill adds, is AI that watches everyone at once and can “scan everything you do in every way, shape, or form.”

Add it up and you get money that can be programmed — money that, in Maria’s words, can be “tracked, frozen, or switched off.” Picture your card declined at the checkout not because you’re broke, but because someone flipped a switch. Whether or not it lands that way, their warning is one line: the crash isn’t the end of the story. It’s the excuse.

That’s the trap. The one thing still in your hands is how to stay out of it.

Here’s what changes everything: you don’t have to be in this bet.

Sitting in the market as-is, Bill says, is “a passive choice if you’re staying where you’re at, but not one that you have to continue making.” You can walk out the moment you decide to.

His alternative is the oldest one there is. Gold and silver have thousands of years of value behind them; AI, he notes, is “purely speculative” — a few years old, with no idea what it finally produces. Gold, meanwhile, “has held its value through every currency change.” Silver has a twist: it’s the metal they need to build the AI everyone’s chasing. If AI booms, silver climbs because the data centers eat it up. If AI busts, gold does what gold always does. Heads or tails, you’re covered.

Then Maria adds the part people skip: this isn’t only about money. Leave your retirement where it sits and you’re “funding with your retirement a surveillance state” — paying, out of your own paycheck, to build the grid they’d use to track you. For a lot of people, that lands harder than any chart.

The one thing in the way is usually a person: your broker. Most won’t offer physical metal — they keep you in paper they control, and they’ll push back. People tell Bill they’re scared to even bring it up because their advisor will be upset. His answer: “it’s not their money. This is your money.” And: “I think people need to take a hands-on approach to their finances and be empowered.”

Which is where a lot of people are right now — done with the bet, unsure of step one. Step one is simpler than you’d expect.

#ad: Let me ask you something uncomfortable.

Have you ever hesitated to tell your financial advisor what you actually want to do with your own money?

Maybe you’ve already bought a little gold and silver. But your IRA? Your 401(k)? Those accounts are still on autopilot. And right now, autopilot means loaded up on AI stocks at the most concentrated valuations in market history.

So why haven’t you brought it up?

Here’s what Bill at Genesis Gold Group hears all the time: “I don’t want to tell Bob. Bob’s going to get upset.”

Think about what that sentence actually means. People afraid to tell their broker what they think they should do... with their own money.

How backwards is that?

It’s not Bob’s retirement. It’s not Bob’s savings. And Bob pushes back because fund managers don’t sell physical gold and silver. They sell paper assets. The ones they control. The ones they collect fees on. Of course, they want to keep your money in-house.

Nobody is responsible for stewarding your money except you. Not your broker. Not your fund manager. You.

That’s what Genesis Gold Group’s philosophy is built on: you being in control of your own money. They’re not there to talk you into anything. They’re there to empower you to make your own decision about physical gold and silver, including inside your IRA or 401(k).

So here’s the first step: Go to dailypulsegold.com and get the free guide.

It covers what’s really at stake, from the AI bubble to the coming digital ID system, and exactly how physical gold and silver work inside a retirement account.

Read it. Then have a conversation with Bill and ask him anything. Have the conversation Bob doesn’t want you to have.

It’s your money. Act like it. Dailypulsegold.com.

DISCLOSURE: This ad was paid for by Genesis Gold Group. We may earn a small commission when you shop through our sponsors. Thank you for your support.

We want to thank Bill Armour for joining us today—and more importantly, we want to thank you for watching and doing your duty to be informed when so many others choose not to.

Follow us (@ZeeeMedia and @VigilantFox) for stories that matter—stories the media doesn’t want you to see.

We’ll be back with another show on Friday. See you then.